How to Dollar Cost Average (DCA) in Crypto: Full Strategy for 2026

Dollar cost averaging (DCA) in crypto means buying a fixed dollar amount on a set schedule, no matter what the price is.

Crypto prices can jump and drop fast, sometimes in the same week. DCA fits this kind of market because it reduces the pressure to “buy the dip” or guess the next top. It’s simple, but it’s not mindless. For 2026, you still need a plan for what you’ll buy, how often, how you’ll handle fees, how you’ll store coins, and how you’ll track taxes.

This guide is for beginners who want long-term habits, not quick trading wins.

Key Takeaways

- Dollar cost averaging (DCA) in crypto means buying a fixed dollar amount on a set schedule, no matter the price.

- DCA can lower stress and reduce bad timing decisions in a volatile market, but it doesn’t prevent losses.

- DCA works best with a multi-year timeline, money you won’t need soon, and assets you can hold through drawdowns.

- Weekly, biweekly, or monthly buys all work, choose the schedule that fits your paycheck and keeps fees reasonable.

- A simple beginner setup is a BTC and ETH core, automated recurring buys, basic security steps, and clean tax records.

Crypto DCA basics in 2026: what it is, why it works, and when it fails

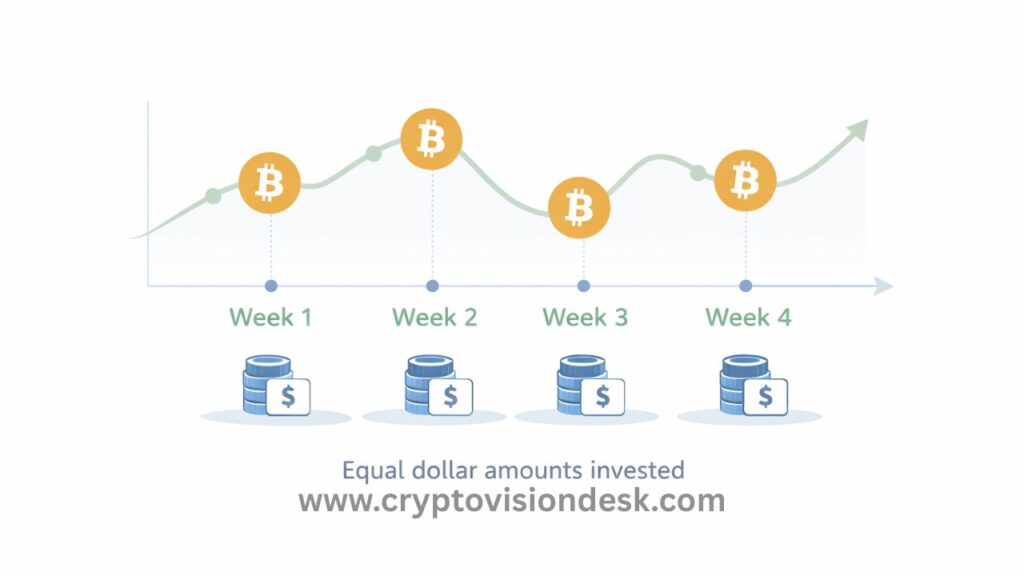

DCA is straightforward: you invest the same amount (like $50 or $200) at the same interval (like every Friday). Over time, you end up buying more when prices are lower and less when prices are higher, which can lower your average entry price compared to random lump buys.

The main benefit is emotional. DCA helps you stop treating every price move like an emergency. When Bitcoin or Ethereum swings hard, your plan keeps running, and your decisions get calmer.

The main limit is also simple: DCA doesn’t prevent losses. If crypto enters a long bear market and prices trend down for a year or two, your portfolio can still be down for a while. DCA helps you keep buying through that period, but you need the time and patience to let it work.

DCA works best when:

- You have a multi-year horizon.

- You’re buying assets you’d feel fine holding for years.

- You’re using money you won’t need for rent, bills, or emergencies.

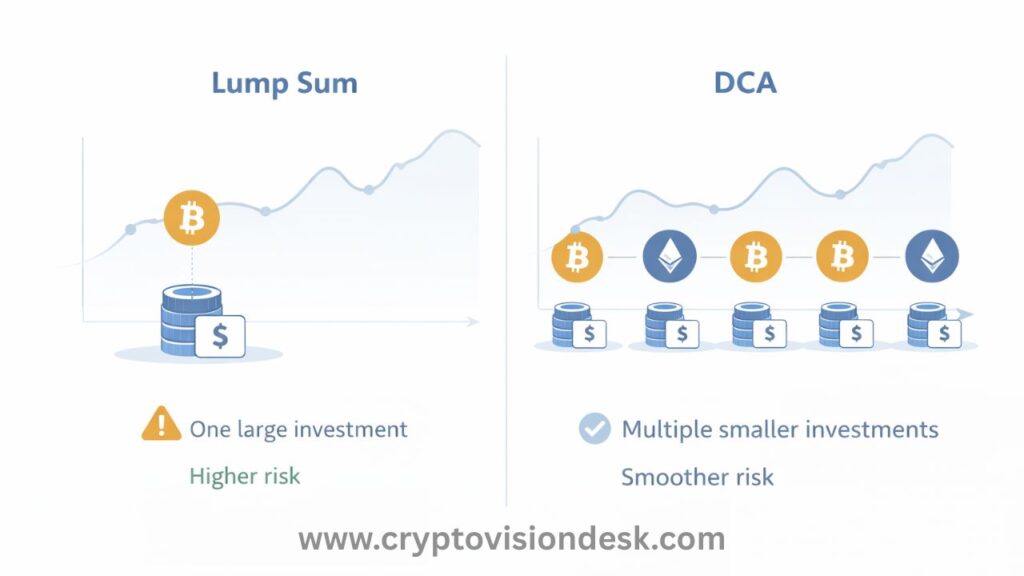

DCA vs lump sum: which one should beginners use?

Lump sum investing means you invest all the money at once. If prices rise soon after you buy, lump sum can outperform DCA because more of your money was in the market earlier.

Crypto doesn’t behave like a calm market, though. Big moves can happen quickly, and that’s where DCA often feels better for beginners. It can lower regret, because you didn’t bet everything on one day’s price.

A simple rule of thumb:

- If you’d be upset if your buy dropped 20 percent next week, start with DCA.

- If you already have strong conviction, a long timeline, and you won’t panic, lump sum can be fine.

Many people also blend both: invest a smaller lump sum to get started, then DCA the rest over months.

Common DCA myths that cost people money

Myth 1: DCA guarantees profit.

DCA improves your process, not your outcome. If the asset performs poorly over years, DCA won’t save it.

Myth 2: DCA is only for bear markets.

DCA is for volatility. It can help in up markets and down markets, because you avoid waiting for a “perfect” entry that never comes.

Myth 3: You should stop buying when price drops.

A drop is often the moment your plan is most useful. If you stop buying only because price fell, you turn DCA into panic timing.

Myth 4: You should chase hot coins with your DCA.

DCA works best when the plan is boring. Rotating your DCA into whatever is trending turns it into performance chasing.

Myth 5: You don’t need a plan to sell.

Buying is only half the job. Without an exit plan, people hold through big gains, then watch them fade because they never decided what “enough” looked like.

Build your crypto DCA plan step by step (amount, schedule, coins, and rules)

Think of DCA like a thermostat, not a lottery ticket. You set it once, check it now and then, and let it run.

Start with basics that keep you safe: have an emergency fund first, pay off high-interest debt, and only invest money you can hold long term.

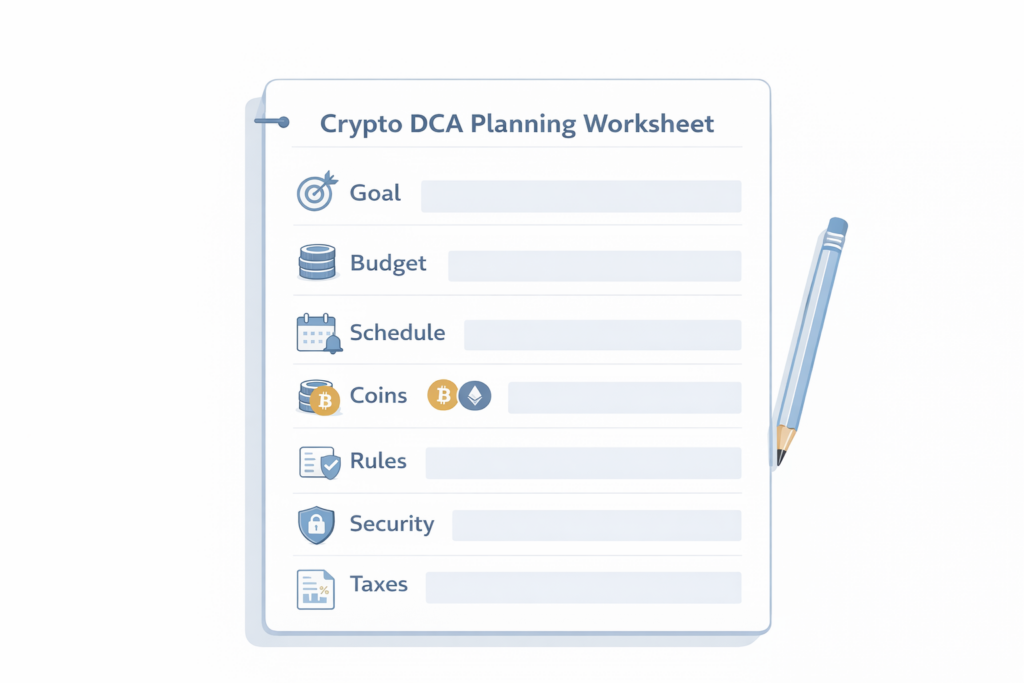

Here’s a simple worksheet you can copy into a notes app:

| Step | Decision | Your answer (example) |

|---|---|---|

| Goal | Why are you buying crypto? | Long-term savings, 5+ years |

| Budget | How much can you buy regularly? | $200 per month |

| Cadence | Weekly, biweekly, or monthly? | Biweekly |

| Coins | What assets will you DCA into? | 70% BTC, 30% ETH |

| Rules | What would make you change the plan? | Income change, fees too high |

| Automation | How will you run it hands-off? | Recurring buys + alerts |

| Security | Where will you store long-term holds? | Hardware wallet after $1,000 |

| Taxes | How will you track cost basis? | Export CSV monthly |

The goal is to remove daily decision-making. If you have to “feel confident” every time you buy, you won’t stay consistent.

Choose your DCA budget and cadence (weekly vs biweekly vs monthly)

Pick a budget that won’t force you to quit when life gets busy. A smaller amount that you can keep doing beats a bigger amount you cancel after two months.

Common cadences:

- Weekly: Good for steady income and building the habit. It can smooth volatility well.

- Biweekly: Matches many paychecks, often a practical sweet spot.

- Monthly: Simple, fewer transactions, and often lower total fees.

The key is to keep the buy size fixed. If your plan is $100 every Friday, it stays $100, even after a green week. That’s what stops emotional decision-making from sneaking back in.

Fees matter more than many beginners expect. Smaller, more frequent buys can increase total fees on platforms that charge a fixed or percentage fee per transaction. Spreads can also sting on tiny trades. If your platform isn’t fee-friendly, biweekly or monthly buys can be a smarter setup.

A clean way to sanity check your budget:

- If you had to pause your DCA for 3 months, would your life be fine?

- If not, the budget is too high.

Pick what to DCA: a simple beginner portfolio approach (core and small extras)

A beginner DCA plan should be easy to follow during chaos. That usually means a core position in large, liquid assets, then optional small “extras” if you really want them.

For many long-term investors, the core is Bitcoin and Ethereum because they’re widely traded, widely held, and supported across most reputable platforms. They’re still risky, but they’re generally less fragile than low-cap coins.

A simple structure:

- Core (80 to 100 percent): BTC, ETH, or a mix

- Satellites (0 to 20 percent): one or two higher-risk picks you understand

Avoid making meme coins the foundation of your DCA. You can’t build a steady plan on assets that can drop 60 percent on a rumor.

If you want simplicity, limit the number of coins. One to three is enough for most beginners. Fewer choices means fewer second guesses.

Here are example allocations (not promises, just templates):

| Style | Coins | Example split |

|---|---|---|

| Ultra-simple | BTC only | 100% BTC |

| Balanced core | BTC + ETH | 70% BTC, 30% ETH |

| Core + small extras | BTC + ETH + 1 alt | 60% BTC, 30% ETH, 10% alt |

Set it up safely: platforms, automation, storage, and tax basics

Your strategy is only as strong as your setup. The “best” DCA plan on paper falls apart if you pick a platform with confusing fees, weak security, or no exportable records.

When choosing an exchange or brokerage for crypto DCA, look for:

- Recurring buys that are easy to control

- Transparent fees, including spreads

- Strong account security options (2FA, device approval)

- Clear deposit and withdrawal rules

- A way to export transaction history for taxes

Many beginners start on major exchanges that offer recurring buys (for example, Coinbase, Binance, or Kraken), then later move long-term holdings into a wallet. What matters most is that the platform is reputable in your region and fits your fee and security needs.

Taxes are part of the plan, even if you hate spreadsheets. In many countries, buying isn’t taxed, but selling is. Each DCA buy creates a new “lot” with its own cost basis, which is why recordkeeping matters.

Basic tax habits that save time later:

- Download or export your transaction history monthly.

- Track transfers between exchange and wallet (they’re often not taxable, but they must be documented).

- Know your local capital gains rules (holding period rules can change the rate).

- Consider using crypto tax software if you trade across many wallets and platforms.

How to automate DCA (recurring buys, auto-invest, and simple bots)

Automation is the point. If you’re still manually buying each time, your mood will sneak into the plan.

The easiest path is built-in recurring buys on your chosen platform. Set the amount, set the cadence, and fund it from your bank balance. Then add a calendar reminder to check that buys are still executing.

More advanced users sometimes use third-party bots or API tools to place scheduled orders. If you go that route, be strict:

- Use limited API permissions (trading only, no withdrawals if possible).

- Use strong account security.

- Treat bot access like a spare key to your house.

If automation makes you sleep better, it’s doing its job.

Security checklist: 2FA, withdrawal safety, and when to move coins to a wallet

Security mistakes are a brutal way to learn. A good DCA plan includes a simple safety routine.

A beginner-friendly checklist:

- Enable 2FA with an authenticator app (avoid SMS when possible).

- Use a long, unique password, and store it in a password manager.

- Watch for phishing, fake support accounts, and cloned websites.

- Turn on withdrawal address whitelists if your platform offers it.

- Don’t keep a large long-term balance on an exchange.

- Consider moving long-term holdings to a hardware wallet once your balance is meaningful to you.

Self-custody is a tradeoff. When you move coins to your own wallet, you remove exchange risk, but you take on personal responsibility. If you lose your recovery phrase, there’s usually no rescue button. Write your recovery phrase down, store it securely, and never share it.

Staying on track in 2026: review schedule, rebalancing, and an exit plan

DCA can feel boring, and that’s a feature. The danger is checking prices too often and “improving” your plan every time crypto gets noisy.

Set a review schedule that fits real life:

- Quick check every 1 to 3 months

- Deeper review once or twice per year

During your review, ask a few plain questions:

- Am I still able to afford this DCA amount?

- Are fees still reasonable?

- Did my allocation drift too far?

- Do I still understand and believe in what I’m buying?

Rebalancing is a simple way to keep risk under control. If your target is 70% BTC and 30% ETH, a strong ETH run could push you off target. Rebalancing means trimming what grew faster or directing new contributions toward what fell behind.

You also need an exit plan. Not because you’re trying to time the top, but because “I’ll figure it out later” often turns into no action at all.

When to change your DCA plan (and when not to)

Good reasons to change your plan:

- Your income changed, and the DCA amount no longer fits.

- You notice fees eating a painful share of each buy.

- You picked too many coins and stopped following the logic.

- You want to reduce risk as your portfolio grows.

Bad reasons to change your plan:

- A scary headline.

- A bad week.

- A friend bragging about a new coin.

- A sudden need to feel “certain” before buying.

One of the most common DCA failures is panic stopping. The whole point is to keep your behavior steady while the market is not.

Simple profit-taking ideas and risk limits (without trying to time the top)

Taking profit doesn’t have to mean selling everything. It can mean setting rules that stop you from round-tripping life-changing gains.

Here are three beginner-friendly approaches:

Milestone sells: Sell a small percentage at pre-set gains (example, trim 10% after a big move, then another 10% later). You’re not calling the top, you’re paying yourself in stages.

Rebalance to targets: If your crypto allocation grows beyond your comfort level, rebalance back to your planned mix. This can act like “sell some high” without guesswork.

Time-based goals: If your plan is a 5-year hold, set a review date and decide then, based on your life and finances, not on today’s chart.

Pair profit-taking with risk limits that keep you stable:

- Set a max crypto allocation for your net worth (many people choose a cap so one crash won’t wreck them).

- Keep an emergency fund in cash.

- Don’t borrow money to DCA.

- Don’t raise your DCA amount just because prices are pumping.

Read Also: How To Earn Money With Crypto in 2026: 7 Safe Ways

Frequently Asked Questions About Crypto Dollar Cost Averaging (DCA)

What is crypto DCA, and how does it work?

Crypto DCA is a plan where you buy the same dollar amount of crypto on a set schedule (for example, $100 every Friday). Over time, you buy more when prices are low and less when prices are high, which can improve your average entry price versus random buys.

Is DCA better than lump sum investing in crypto?

Lump sum can perform better when prices rise soon after you invest, because more money is invested earlier. DCA often works better for beginners because it reduces regret and removes the pressure to pick the perfect day in a market that moves fast.

How often should I DCA into crypto (weekly, biweekly, or monthly)?

Weekly works well for habit building and smoothing swings. Biweekly matches many paychecks and can be a practical middle ground. Monthly keeps it simple and can reduce total fees, especially if your platform charges per trade or has wide spreads.

What coins should beginners DCA into?

Many beginners keep the plan simple with a core in Bitcoin and Ethereum because they are widely traded and supported by most major platforms. If you add extra coins, keep them small (often 0 to 20 percent total) and limit your list to one or two so you don’t chase trends.

What are the biggest mistakes people make with crypto DCA?

Common mistakes include thinking DCA guarantees profit, stopping buys after a drop, chasing hot coins, and skipping an exit plan. DCA is about steady behavior, it still needs rules for fees, security, reviews, and profit-taking.

Is crypto DCA safe for beginners?

Crypto DCA is safer than trying to time the market, but it is not risk-free. Prices can still fall for long periods. DCA works best for beginners who invest small amounts consistently and plan to hold for the long term.

How much money should beginners invest using crypto DCA?

Beginners should start with an amount they can afford to invest regularly without financial stress. Even small amounts like $25–$100 per month can be effective if invested consistently over several years.

Is weekly or monthly DCA better for crypto investing?

Weekly DCA reduces volatility more effectively, while monthly DCA lowers fees and effort. Both work well. The best option is the schedule you can follow consistently without skipping or adjusting based on market emotions.

Should beginners DCA only into Bitcoin?

Many beginners choose Bitcoin or a Bitcoin and Ethereum combination because they are more established and liquid. Smaller altcoins are riskier and should only be added in small amounts after proper research.

Can Dollar Cost Averaging fail in crypto?

Yes. DCA does not guarantee profits. If a crypto asset performs poorly over many years, DCA will not prevent losses. It improves discipline and risk management, not market performance.

Is DCA better than lump sum investing in crypto?

DCA is often better for beginners because it reduces emotional stress and regret. Lump sum investing can outperform when prices rise quickly, but DCA offers smoother entry during volatile market conditions.

When should I stop or change my crypto DCA plan?

You should change or pause your DCA plan if your income changes, fees become too high, or crypto becomes too large a portion of your net worth. Short-term price drops are not a good reason to stop DCA.

Do I need to pay tax on crypto DCA purchases?

Buying crypto through DCA is usually not taxable. Taxes generally apply when you sell, swap, or use crypto. Each DCA purchase creates a separate cost basis, so tracking transactions is important.

Should I keep DCA crypto on an exchange or move it to a wallet?

Long-term investors often move DCA holdings to a personal wallet for better security. Exchanges are convenient but carry platform risk. Self-custody gives more control but requires careful key management.

Can crypto DCA be fully automated?

Yes. Most major crypto exchanges offer recurring or automated purchase options. Automation helps maintain consistency and removes emotional decision-making from your investment process.

Is crypto DCA good for short-term profits?

No. Crypto DCA is designed for long-term investing, not quick profits. It works best over multiple years, allowing time for market cycles to play out.

How should beginners take profits when using DCA?

Beginners can take profits gradually by selling small portions at predefined levels, rebalancing their portfolio, or reviewing holdings after a fixed time period instead of trying to time the market top.

Conclusion

A strong crypto DCA strategy for 2026 is simple, but it’s not sloppy. Keep it focused:

- Pick a goal and a timeline you can stick to.

- Build a BTC and ETH core (keep extras small, if any).

- Set a fixed amount and schedule you can afford.

- Automate recurring buys so emotions don’t run the show.

- Secure your account, track taxes, and review monthly.

Start small this week, set recurring buys, and check in once a month. In crypto, patience and consistency beat perfect timing.

Read Also: Best Crypto Apps For Android (2026), Safe Beginner Picks

Disclaimer

The information provided on this website is published in good faith and for general informational and educational purposes only. It does not constitute financial, investment, trading, legal, or tax advice of any kind.

Cryptocurrencies and digital assets are highly volatile and involve substantial risk. Market conditions can change rapidly, and users may lose some or all of their invested capital. Any actions taken based on the information found on this website are strictly at the reader’s own risk.

References to cryptocurrencies, exchanges, wallets, tools, platforms, or strategies are shared solely for educational awareness and should not be interpreted as recommendations, endorsements, or professional advice.

Readers are advised to conduct their own research (DYOR) and seek guidance from a qualified financial advisor, tax consultant, or legal professional before making any financial or investment decisions.

Cryptocurrency laws, regulations, and taxation policies—particularly in India—may change over time. The content on this website is based on publicly available information at the time of publication and may not reflect the most recent legal or regulatory updates.

The website owner, authors, and contributors do not accept any liability for losses, damages, or consequences arising from the use of the information provided on this website.

Some content on this website may contain affiliate links. This means we may earn a small commission at no additional cost to you. This does not influence the accuracy, transparency, or integrity of the content.