Crypto Tax in India (2026 Guide), Calculate Gains, Claim 1% TDS, Reduce Losses Legally

Crypto profits can feel simple until you try to file your return and hit India’s VDA tax rules. For FY 2025-26 (AY 2026-27), crypto and NFTs follow a separate set of rules, and small tracking mistakes can mean paying more than you should.

India taxes profits from Virtual Digital Assets (VDAs) at a flat 30% rate (plus surcharge and 4% cess). You can only subtract the cost of buying the asset, and VDA losses have strict limits, they generally can’t be set off against other income or carried forward.

This beginner-friendly 2026 guide breaks it down in plain steps. You’ll learn what counts as a taxable crypto transfer, how to calculate gains trade by trade, and how the 1% TDS works (including how to claim the credit through your ITR and Form 26AS).

You’ll also see legal ways to reduce losses and avoid overpaying, mainly by better record-keeping, clean reporting, and planning trades within the rules. Tax rules can change, so double-check the latest CBDT updates, and speak to a CA for complex cases like staking, overseas exchanges, or high-volume trading.

Crypto tax in India for 2026, the rules you must know before you calculate anything

Before you open a spreadsheet or a tax calculator, you need the ground rules. India’s crypto tax system is built around two ideas: what counts as a Virtual Digital Asset (VDA), and what counts as a transfer. If you get these wrong, your “profit” number can be off, and your tax filing can turn messy fast.

At a high level, buying and holding is quiet, but moving crypto from you to someone else (for money, for another coin, or for a product) is where tax usually shows up.

What counts as a VDA, and what actions trigger tax (sell, swap, spend, gift)

A VDA mainly includes:

- Crypto tokens/coins (like BTC, ETH, SOL, and stablecoins)

- NFTs (and similar tokenized digital assets)

The key point is that tax under the VDA rules is tied to a transfer, not to price going up and down while you hold.

Here are the common actions that trigger VDA tax, because each one is treated as a transfer:

- Sell for INR (or any fiat): You sell crypto and receive rupees. This is the simplest taxable case.

- Swap coin to coin: You trade one crypto for another (for example, ETH to USDT, BTC to SOL). Even if no INR hits your bank, it still counts as a taxable transfer.

- Spend crypto: You use crypto to buy goods or services. Think of it like bartering, you paid with a token instead of cash, so it’s still a transfer.

- Gift crypto or NFTs: Giving a VDA to someone can count as a transfer. Also, gift taxation can differ based on who receives it (relative vs non-relative) and the fair market value of the gift. If you’re gifting anything meaningful in value, get professional advice so you report it the right way.

What does not trigger VDA tax on its own?

- Holding: If you buy and simply hold, there’s no transfer, so there’s no VDA profit tax at that moment. Your tax point usually comes later, when you sell, swap, spend, or gift.

If you remember one mental model, use this: no transfer, no VDA tax calculation yet.

The 30% tax rule under Section 115BBH, plus surcharge and 4% cess

Once you have a taxable transfer, Section 115BBH sets a flat tax rate on the profit. There’s no special reward for holding longer. It’s the same rate whether you held for two days or two years.

- Tax rate: 30% on profits from transferring VDAs

- No short-term vs long-term benefit: The 30% rate applies either way

- Effective tax can be higher: You also add surcharge (if your total income crosses certain thresholds) and the 4% health and education cess

Use this simple formula as your starting point:

Tax = 30% of VDA profit, then add surcharge (if applicable), then add 4% cess on the total tax + surcharge.

A quick example makes it real. If your profit from a transfer is ₹1,00,000:

- Base tax at 30% = ₹30,000

- Add surcharge (only if your total income makes it applicable)

- Add 4% cess on (tax + surcharge)

This is why two people with the same crypto profit can pay different final tax amounts, the 30% is fixed, but the extras depend on total income.

How to calculate crypto gains and tax in India, step by step (with a simple example)

For India’s VDA rules, don’t overthink it. Treat each taxable transfer (sell, swap, spend) like a mini profit and loss statement. Your job is to (1) find the INR value on the transfer date, (2) subtract what you paid to buy that exact crypto, and (3) repeat trade by trade using your exchange statements.

A simple workflow that works for most people:

- Export your trade history from each exchange (and keep contract notes, if available).

- For every transfer, write down: date/time, coin, quantity, INR value at that moment, and buy cost.

- Compute gain per transfer, then total them for the year.

- Match your 1% TDS with Form 26AS before you file.

The basic formula for each trade: sale value minus cost (what you can and cannot deduct)

Under the VDA regime, the core math stays simple:

Gain per transfer = Sale consideration (INR value received) minus Cost of acquisition

What counts in practice:

- Sale consideration: The INR value you got when you transferred the crypto.

- If you sold for INR, it’s the INR proceeds.

- If you swapped or spent crypto, it’s the INR fair value at that time (more on this below).

- Cost of acquisition: What you paid to buy that crypto (in INR terms).

- If you bought with INR, use the buy value from your exchange statement.

- If you acquired it in parts, keep the buy records for each lot.

What you generally cannot deduct under Section 115BBH (so don’t assume it reduces tax):

- Exchange fees, brokerage, platform charges

- Gas fees, network fees, transfer fees

- Charting tools, subscriptions, “advisory” fees

- Any other “business” or “misc” costs linked to trading

That’s why record-keeping matters more than clever math. Keep these proofs:

- Buy confirmation and price (trade receipt, statement export)

- Fee lines shown in statements (even if you can’t deduct them, they help you reconcile totals)

- Exact timestamps (important for swaps, where price moves fast)

- Wallet and exchange records (deposits, withdrawals, and internal transfers)

If you only keep one habit, keep this one: every sell must point back to a buy (same coin, correct quantity).

How to handle common cases: INR sell, crypto to crypto swap, and buying something with crypto

Different trade types look different on the app, but the tax logic is the same: treat it as a transfer and translate it into INR on that moment.

1) Sell crypto for INR

This is the cleanest case.

Method

- Sale value = INR you received (as per the exchange trade confirmation)

- Cost = INR you paid when you bought that coin

- Gain = Sale value minus cost

- Tax = 30% of gain (then surcharge, if applicable, plus 4% cess)

Mini example (sale)

- You buy 0.01 BTC for ₹20,000

- Later you sell 0.01 BTC for ₹28,000

Gain = ₹28,000 minus ₹20,000 = ₹8,000

Base tax (ignoring surcharge/cess for simplicity) = 30% of ₹8,000 = ₹2,400

2) Crypto to crypto swap (example: ETH to USDT)

Swaps confuse people because no INR hits your bank. Tax still applies because you transferred a VDA.

Method

- Treat the coin you give up as “sold”

- Sale value = INR value of what you received (or INR value of what you gave up) at the swap time

- Cost = INR cost of acquiring the coin you gave up

- Compute gain on the first coin, and start a new cost basis for the coin you received

Mini example (swap)

- You bought 1 ETH earlier for ₹1,50,000

- You swap 1 ETH for 2,000 USDT

- At that exact time, 2,000 USDT is worth ₹1,80,000 (use your exchange’s INR value or a consistent price source)

Gain on ETH transfer = ₹1,80,000 minus ₹1,50,000 = ₹30,000

Base tax (before cess/surcharge) = 30% of ₹30,000 = ₹9,000

Now set your new cost for what you received:

- Cost of 2,000 USDT becomes ₹1,80,000 (so future gains on USDT start from here)

Consistency tip: Pick one price source and stick to it for the year (your exchange’s executed trade INR value is easiest). If you mix sources, your numbers won’t tie out.

3) Buying something with crypto (spending)

If you pay with crypto, it’s treated like you sold crypto for the INR value of what you bought.

Method

- Sale value = INR value of the item/service you purchased (or INR value of crypto at payment time)

- Cost = what you paid to acquire that crypto

- Gain = Sale value minus cost

This feels like paying with a foreign currency note. You didn’t “sell” it in your head, but for tax you exchanged it for something of value.

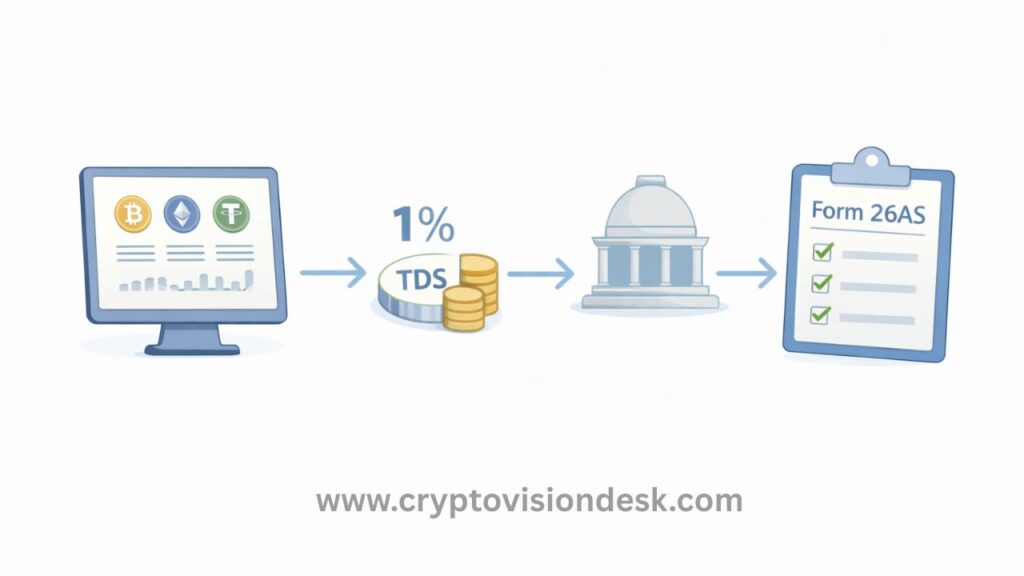

How the 1% TDS works in 2026, thresholds, and how to claim it back in your ITR

India’s crypto TDS is designed to track transfers. It often shows up as many small cuts, which can look scary, but the key idea is simple:

1% TDS is not extra tax. It’s a tax credit.

When TDS applies (the practical view)

- TDS is deducted on the transfer value (the sale amount), not on profit.

- It applies when your transfers cross the annual threshold:

- ₹50,000 in many cases

- ₹10,000 in some cases (depending on your profile, so verify your category before assuming the higher limit)

On many Indian exchanges, TDS is auto-deducted at the time of sell or swap. In P2P or off-exchange transfers, the buyer may have the duty to deduct and deposit TDS, which is where people slip up.

How to claim TDS back (or adjust it) in your ITR

Treat TDS like an advance payment already sitting with the government.

Do this before filing:

- Check your exchange’s TDS statement or transaction history.

- Match the TDS entries with Form 26AS (and AIS, if needed).

- When you file, report your VDA gains, then claim the TDS credit so your final payable tax reduces.

If your total tax on crypto (plus other income) is less than the TDS already deducted, you can end up with a refund, assuming everything matches.

How to report crypto in Schedule VDA, and which ITR form usually fits beginners

For FY 2025-26 (AY 2026-27), crypto reporting goes into Schedule VDA. Think of it as the section where you show the tax department your trade-by-trade profit logic, instead of one lump sum number.

What you should be ready to report cleanly:

- Date of acquisition and date of transfer

- Sale value (INR)

- Cost of acquisition (INR)

- Gain from each transfer (or totals grouped as the schedule allows)

- Any 1% TDS linked to those transfers (as per 26AS)

Which ITR form fits most beginners?

A simple rule of thumb helps:

- ITR-2: Often used by investors who buy and sell as an investment activity.

- ITR-3: More likely if your activity looks like business income (very frequent trading, systematic activity, or you’re clearly operating like a trader).

Don’t guess if your situation has extra layers. Get help if you have staking rewards, mining, airdrops, gifts, overseas exchanges, or a very high trade count, because the “value on receipt” and reporting can change, even when the 30% transfer tax stays the same.

How to reduce losses and avoid overpaying tax, legally (what works, what does not)

When crypto prices swing, it’s normal to look for ways to “use losses” and lower your tax bill. In India, that idea doesn’t work the same way it does for stocks. With VDAs, the rules are strict and they change what good planning looks like.

The best legal approach is simple: avoid taxable transfers you don’t need, calculate gains correctly, and make sure every rupee of 1% TDS shows up as credit in your return. That’s where most real savings come from.

Understand the hard part: VDA losses usually cannot offset other income and cannot be carried forward

Under Section 115BBH, VDA losses generally can’t be set off against other income such as salary, interest, rent, or equity gains. They also cannot be carried forward to future years.

What this means in plain terms:

- If you made a profit on Coin A and a loss on Coin B, you don’t get to “net them off” in the way many people expect.

- Selling a losing coin to reduce tax on salary or stock profits won’t help under the VDA loss rules.

- Each profitable transfer can still get taxed at 30% (plus surcharge and cess) even if you lost money elsewhere in crypto.

Think of it like separate buckets that don’t mix. Your salary bucket is taxed under slab rates, your equity bucket follows capital gains rules, but the VDA profit bucket stands alone and the law blocks the usual loss adjustments.

A practical example:

- You book a ₹1,00,000 profit by selling BTC.

- You also book a ₹1,00,000 loss by selling an altcoin.

- You might expect your net crypto profit is zero, but under VDA rules, the BTC profit can still be taxed, and the altcoin loss doesn’t rescue it.

So the goal shifts from “loss harvesting” to damage control: reduce avoidable taxable events, prevent reporting errors, and claim the credits you already paid.

Legal ways to reduce damage: delay transfers, use accurate cost records, and claim every TDS credit

You can’t wish away VDA tax, but you can stop overpaying. These three levers are realistic, legal, and useful for most investors.

1) Timing: tax happens on transfer, so holding can defer tax

VDA tax is linked to a transfer (sell, swap, spend, gift). If you don’t transfer, you generally don’t trigger the 30% tax calculation at that moment.

What works here:

- If you were about to sell only because of fear or hype, pausing can also pause the tax event.

- If you plan to rebalance, consider whether you really need to swap this year or if it can wait.

What doesn’t work:

- Pretending a transfer is “internal” when it’s actually a trade, a swap, or a spend.

- “Parking” funds through complicated steps that still include taxable swaps. More steps often means more taxable transfers.

2) Accuracy: clean cost records stop you from paying tax on the wrong gains

Many people overpay because their cost basis is wrong. This happens when you move coins across wallets and exchanges and your buy history gets lost, or when you rely on a single exchange app that only shows partial history.

To keep it correct, treat your records like a chain of custody:

- Wallet to exchange transfers: These are usually not taxable by themselves, but they can break your records. Always link the deposit to the original buy.

- INR value at buy time: Cost is what you actually paid. If you bought in parts, track each lot.

- Fees shown: Even if fees are not deductible under 115BBH, they help reconcile why your balances and proceeds don’t match perfectly across statements.

If your cost is missing, you might end up reporting too much gain. That’s the easiest way to overpay.

3) Claim every 1% TDS credit so you don’t pay twice

The 1% TDS on VDA transfers is designed to track trades. It often gets deducted on the full sale value, even when your profit is small.

If you forget to claim it, you can end up paying:

- TDS during the year, and

- full self-assessment tax again at filing time.

Make it a habit:

- Match exchange TDS reports with Form 26AS (and AIS, if needed).

- Claim the TDS credit in your ITR when you report VDA income in Schedule VDA.

- If TDS is missing in 26AS, follow up early with the exchange or deductor. Waiting until the last week makes it harder.

Quick record checklist (keep this before you even start calculations)

Keep these items in one folder per financial year. It saves hours later and reduces mistakes.

- Exchange CSV exports for each platform (trades, deposits, withdrawals)

- Order-wise confirmations or contract notes (if available)

- Blockchain transaction IDs (TXIDs) for wallet transfers

- Screenshots or PDFs of key fills (large trades, P2P confirmations)

- INR values used for each taxable transfer (as shown by the exchange at execution time, or a consistent source if you must self-compute)

- Dates and timestamps (especially for swaps)

- TDS entries (exchange statement plus Form 26AS match)

Staking, airdrops, mining, salary in crypto, and rewards, how they may be taxed differently

Not all crypto you receive starts as a “purchase”. If you got tokens through staking, an airdrop, mining, referral rewards, or as salary, there can be two tax moments:

- At receipt: It may be treated as income (often taxed at slab rates) depending on the facts and how it’s classified.

- At transfer later: When you sell or swap that crypto, it can trigger VDA transfer tax rules again, where profits are taxed at 30% under Section 115BBH.

High-level treatment (the exact head can depend on your situation):

- Staking rewards and similar yields: Often treated like income when you receive the reward, then taxed again under VDA rules when you later transfer the tokens (based on sale value minus allowable cost basis).

- Airdrops and promotional rewards: Often treated as income at receipt if it’s clearly a benefit you received, then transfer tax when sold.

- Mining: Can involve income characterization issues, plus the VDA transfer tax when you sell mined coins. The facts matter a lot here.

- Salary paid in crypto: Salary is usually taxed under salary rules (based on INR value on the pay date), then when you later sell the crypto, the transfer can create a VDA gain or loss.

To stay safe (and avoid arguing with your own past self at filing time), document the basics for every non-buy receipt:

- Source (staking platform, employer, protocol, campaign)

- Date and time received

- Token and quantity

- INR value on the date of receipt

- Any proof you can download (payout history, email, payslip, on-chain TXID)

If you have sizable staking income, mining activity, or overseas platforms, get a CA to confirm the right classification. Small differences in “when it’s taxed” and “under which head” can change your final number a lot, even when the 30% VDA transfer tax rate stays fixed.

Beginner checklist to stay compliant and avoid notices in 2026

If you want a quiet tax season, treat your crypto taxes like a bank reconciliation. The tax department mostly flags mismatches. That means the safest move is to make your numbers trace back to exchange statements, wallet transfers, and Form 26AS (for 1% TDS). Do this once, cleanly, and you reduce the chance of follow-up questions later.

Before filing: reconcile exchange reports, wallet activity, and Form 26AS (TDS)

Start with a simple rule: your return should match what exchanges and deductors have already reported. Here’s a practical process you can finish in an afternoon if your trades are not too many.

- Download exchange tax reports and full trade history (CSV/PDF)

- Pull the tax report (if the exchange provides one), plus the raw trade history for the full financial year.

- Also download deposit and withdrawal history, not just trades. This helps explain balance changes.

- If you used multiple exchanges, download from each and save them in one folder (one sub-folder per exchange).

- List all wallet transfers (so you can explain movement without “inventing” income)

- Make a simple list of every on-chain transfer you made to or from wallets.

- For each transfer, capture: date, coin, quantity, wallet address, exchange deposit address, and TXID.

- Mark which ones are internal moves (you moving your own coin). These are usually not taxable by themselves, but they often break cost tracking if you don’t document them.

- Match 1% TDS entries with Form 26AS

- Open Form 26AS and filter for TDS related to VDA transfers (often many small lines).

- Match it against your exchange TDS statement or transaction list.

- If TDS shows in the exchange report but not in 26AS, don’t ignore it. Follow up early with the exchange or deductor, because missing credits can create a mismatch and can also delay refunds.

- Do not skip crypto to crypto swaps

- Swaps (like BTC to USDT, ETH to SOL) still count as a taxable transfer under VDA rules.

- Many beginners only report INR sells. That is one of the fastest ways to end up with totals that don’t match platform data.

A quick self-check that catches most issues: your total transfers (sells, swaps, spends) in your records should explain why your holdings dropped, and your TDS total should match 26AS.

Common mistakes to avoid: wrong INR values, double counting, missing fees, and ignoring overseas or P2P trades

Most crypto tax problems are boring data problems, not complex tax problems. Watch out for these common errors, they often trigger mismatches and notices.

- Wrong INR values: Don’t use random Google prices. Use the executed trade value shown by your exchange, or one consistent price source when you must self-value (like for some wallet-only swaps).

- Timezone mix-ups: Exchanges may export in UTC while you track in IST. A few hours can shift a trade into the wrong day, and your swap values can change.

- Double counting the same activity: People count both the exchange trade and the wallet movement as separate taxable events. A withdrawal to your own wallet is not a sale.

- Counting deposits as income: Depositing crypto into an exchange is not income, it’s just movement. Income depends on how you got the crypto (salary, reward, airdrop), not where you store it.

- Missing cost basis (buy cost): If you don’t link every sale or swap back to its buy, you can end up paying tax on inflated gains. Keep the buy lot records intact, even after moving coins.

- Ignoring fees in reconciliation: Under VDA rules, you generally can’t deduct many fees from the taxable gain, but fees still affect balances. If you ignore them, your totals won’t match exchange statements.

- Forgetting crypto to crypto swaps: A swap is still a transfer. If your report only has INR sells, it’s usually incomplete.

- Assuming overseas exchanges mean no reporting: Even if a foreign exchange does not deduct TDS, you still need to compute gains and report them in Schedule VDA.

- Skipping P2P trades: P2P often causes gaps because records are split across chat, bank statements, and the exchange. Keep screenshots, order IDs, and bank proofs together.

- Ignoring small trades: Tiny swaps and partial fills add up. If you trade often, missing even 1% of entries can break the match.

If your trade count is high, or you used multiple exchanges plus wallets plus P2P, get help early. A CA or a reliable crypto tax tool can turn a messy pile of exports into a clean, consistent report. The goal is simple: no missing swaps, no ignored P2P, TDS matched to 26AS, and a clear cost basis. When those four are in place, compliance becomes much less stressful.

Conclusion

Crypto tax in India stays strict for FY 2025-26 (AY 2026-27), so the win is getting the basics right and avoiding avoidable mistakes.

- VDA profits are taxed at a flat 30%, plus surcharge (if it applies) and 4% cess.

- The 1% TDS is a credit, not extra tax, claim it through Form 26AS and your ITR.

- Crypto to crypto swaps, spends, and most transfers are taxable, not just INR sells.

- VDA loss set-off rules are tight, losses usually can’t offset other income or carry forward.

- Clean cost records stop you from paying tax on inflated gains.

Start a clean transaction log today, download exchange statements and TDS reports, reconcile them with Form 26AS, then file using Schedule VDA.

Before you submit, verify any CBDT updates for FY 2025-26, and loop in a CA for complex cases like staking, airdrops, mining, P2P, or overseas exchanges.

Read Also: Best Crypto Apps For Android, Safe Beginner Picks

Do I have to pay tax on crypto in India even if I don’t withdraw to my bank?

Yes. Selling, swapping, or spending crypto is taxable even if no INR is withdrawn. Crypto-to-crypto swaps are also taxable.

Is crypto taxed at slab rates or a fixed rate?

Profits from crypto (VDAs) are taxed at a flat 30% rate, plus surcharge (if applicable) and 4% cess, regardless of your income slab.

Is holding crypto taxable in India?

No. Simply buying and holding crypto is not taxable. Tax applies only when you transfer it (sell, swap, spend, or gift).

How do I calculate crypto profit for tax?

Profit = Sale value (INR) − Cost of buying the crypto.

Only the purchase cost is allowed as a deduction.

Can I deduct trading fees or gas fees from crypto tax?

No. Under current VDA rules, exchange fees, gas fees, and other expenses cannot be deducted.

Can crypto losses be set off against salary or stock market gains?

No. Crypto losses generally cannot be adjusted against any other income and cannot be carried forward.

Is crypto-to-crypto trading taxable in India?

Yes. Swapping one coin for another (e.g., ETH to USDT) is treated as a taxable transfer.

What is 1% TDS on crypto, and is it extra tax?

1% TDS is not extra tax. It is an advance tax deducted on the transaction value and can be claimed back while filing your ITR.

How do I claim 1% TDS on crypto?

You can claim it while filing your income tax return by matching it with Form 26AS and reporting crypto income in Schedule VDA.

Which ITR form should I use for crypto income?

Most investors use ITR-2.

If crypto trading looks like a business activity, ITR-3 may apply.

What is Schedule VDA in income tax retur

Schedule VDA is where you report crypto transactions, including date, asset, cost, sale value, gains, and TDS details.

Do I need to report crypto if I traded on a foreign exchange?

Yes. Crypto income must be reported even if the exchange is outside India and no TDS was deducted.

Is gifted crypto taxable in India?

Yes, depending on who gifted it and its value. Gifts from non-relatives above limits may be taxable.

How are staking rewards or airdrops taxed?

They may be taxed as income when received and again taxed at 30% when sold or swapped. Proper records are important.

What happens if I don’t report crypto income?

Unreported crypto income can lead to notices, penalties, interest, and loss of TDS credit.

Is there any legal way to reduce crypto tax in India?

You cannot reduce the tax rate, but you can avoid overpaying by:

Keeping accurate buy records

Avoiding unnecessary taxable transfers

Claiming full 1% TDS credit

Should beginners consult a CA for crypto tax?

Yes, especially if you have:

Many trades

P2P or overseas exchanges

Staking, mining, or NFT income

Disclaimer

The information provided on this website is published in good faith and for general informational and educational purposes only. It does not constitute financial, investment, trading, legal, or tax advice of any kind.

Cryptocurrencies and digital assets are highly volatile and involve substantial risk. Market conditions can change rapidly, and users may lose some or all of their invested capital. Any actions taken based on the information found on this website are strictly at the reader’s own risk.

References to cryptocurrencies, exchanges, wallets, tools, platforms, or strategies are shared solely for educational awareness and should not be interpreted as recommendations, endorsements, or professional advice.

Readers are advised to conduct their own research (DYOR) and seek guidance from a qualified financial advisor, tax consultant, or legal professional before making any financial or investment decisions.

Cryptocurrency laws, regulations, and taxation policies—particularly in India—may change over time. The content on this website is based on publicly available information at the time of publication and may not reflect the most recent legal or regulatory updates.

The website owner, authors, and contributors do not accept any liability for losses, damages, or consequences arising from the use of the information provided on this website.

Some content on this website may contain affiliate links. This means we may earn a small commission at no additional cost to you. This does not influence the accuracy, transparency, or integrity of the content.