CBDC in India: Digital Rupee Guide 2026 for Everyday Users

If you use UPI every day and maybe hold a bit of crypto on an exchange, you have probably seen the term Digital Rupee (e₹) in the news. It can sound scary or confusing, as if the government will switch off cash one fine day.

That is not what is happening.

The Reserve Bank of India (RBI) is testing a Central Bank Digital Currency, or CBDC, called the Digital Rupee. As of late 2025 it is in pilot mode with a few million users. 2026 is likely to bring wider use, but in a slow and controlled way, not an overnight shock.

This guide keeps things simple. You will see what CBDC means, how e₹ is different from UPI and crypto, how it might show up in your daily spending and small investments, and what risks and myths you should watch.

What Is CBDC and the Digital Rupee (e₹) in Simple Words?

Think of CBDC like RBI-issued cash that lives on your phone instead of your pocket.

CBDC meaning: A quick, clear definition for Indian users

CBDC stands for Central Bank Digital Currency. In India, that is digital money issued by the RBI, with the same value as normal rupees.

The Digital Rupee (e₹) is India’s version of CBDC. If you hold 100 e₹ in a CBDC wallet, it is legally the same as holding ₹100 in physical cash. It is just in electronic form, recorded in RBI’s systems.

Digital Rupee vs physical cash vs bank balance: What is the real difference?

Picture three versions of the same ₹500:

- A ₹500 note in your hand: this is cash. RBI prints it and you hold the paper.

- ₹500 showing in your bank app: this is bank balance. The bank keeps a record in its ledger.

- ₹500 as e₹ in a CBDC wallet: this is Digital Rupee. RBI keeps the record in its digital ledger.

All three are rupees. The key change is who holds the record and where you store it. e₹ is like digital cash backed directly by RBI, stored in a special wallet instead of a bank account.

Retail vs wholesale CBDC in India: What matters for normal people?

RBI is testing two types:

- Wholesale CBDC for banks and big institutions to settle trades and loans.

- Retail CBDC for people like you and me for daily payments.

For a salaried user or small investor, the important one is retail e₹, which you may use in 2026 in your own wallet app.

Digital Rupee Status in 2025 and What to Expect in 2026

RBI is moving in phases, testing first, then slowly scaling.

Current RBI pilots: Where is the Digital Rupee live right now?

Retail and wholesale e₹ pilots started in late 2022 and are still running. By 2025:

- Several public and private banks offer e₹ wallets to selected users.

- A few million users and many merchants are part of the pilot.

- Features under test include QR payments, person-to-person transfers, merchant payments, and some offline transaction options.

Access is still limited. You cannot yet walk into any bank in any city and demand e₹, but coverage is growing.

2026 outlook: How might the CBDC rollout expand in India?

RBI has made its approach clear: slow, step by step.

In 2026, you can expect:

- More banks and fintech apps to add e₹ options.

- Wider city and town coverage.

- More tests of offline features and programmable use cases like targeted subsidies.

RBI has not fixed a final nationwide launch date. Plans depend on tech, law, and operations working smoothly, so ignore rumors that promise exact deadlines.

Will the Digital Rupee replace cash, UPI, or bank accounts?

RBI’s public message is consistent: e₹ will complement cash and UPI, not remove them.

Cash, UPI, cards, and bank accounts are expected to stay. For many users, e₹ will just be one more option for payments, useful in some cases like government transfers or no-network areas.

How the Digital Rupee Will Work for You: Step by Step Use Cases

Think of your normal month: salary, bills, rent, UPI payments, maybe a SIP. e₹ fits into this flow, it does not erase it.

Getting a Digital Rupee wallet: What you may need to do

To use e₹ you will likely:

- Download an RBI-approved wallet app, or use a CBDC feature inside your bank or payment app.

- Complete KYC, just like you did for UPI or your trading account.

- Link your mobile number and set a secure PIN.

There may be limits for small wallets to support financial inclusion and control risk, for example lower caps with lighter KYC.

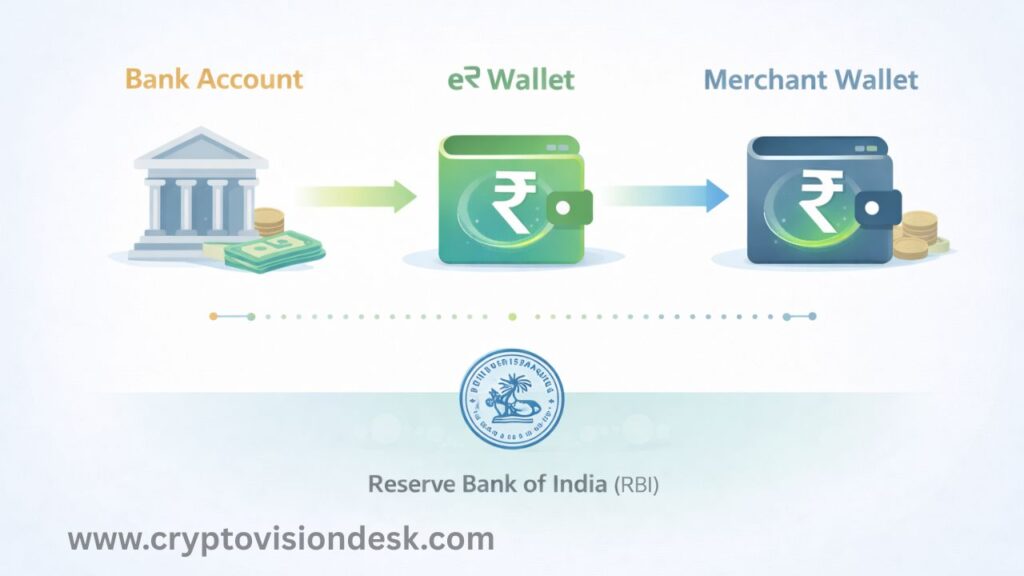

Adding and withdrawing money: From bank account or cash to e₹ and back

Think of moving e₹ as digital withdrawal and deposit:

- You move ₹1,000 from your bank account into e₹. Your bank balance falls by ₹1,000 and your CBDC wallet shows 1,000 e₹.

- Your friend sends you 500 e₹. Your wallet goes up by 500 e₹.

- You send 800 e₹ back to your bank. Your wallet drops by 800, your bank balance rises by ₹800.

The rate is always 1 e₹ = 1 INR. Like cash, e₹ does not earn interest in your wallet.

Paying friends and family with Digital Rupee: Everyday P2P transfers

Imagine you owe a friend ₹300 for dinner.

Today you might use UPI to their bank account. With e₹ you could:

- Open your CBDC wallet.

- Scan their QR or pick their phone number.

- Tap pay, and the 300 e₹ moves instantly from your wallet to theirs.

No need to share bank details. It can feel like passing cash from one hand to another, just on your phone. In some pilots, small offline payments are also tested and sync later.

Shopping and bill payments: Using e₹ with merchants and online apps

In a shop, you might:

- Scan the regular UPI QR using your e₹ wallet, where supported, or

- Scan a special e₹ QR on the counter.

The merchant receives e₹ in their own CBDC wallet. Later, they can move it to their bank account or use it to pay suppliers.

RBI wants retail use to be low cost for users. Any final fee rules will come from RBI and banks, not from random apps.

Government benefits and subsidies: How CBDC could change payouts

e₹ can help with direct benefit transfers. For example:

- A small farmer could receive subsidy straight into a CBDC wallet.

- A worker under a welfare scheme might get e₹ instead of waiting for bank adjustments.

Programmable features can reduce leakage and delay. Exact schemes and rules will depend on future government policy, which is still taking shape.

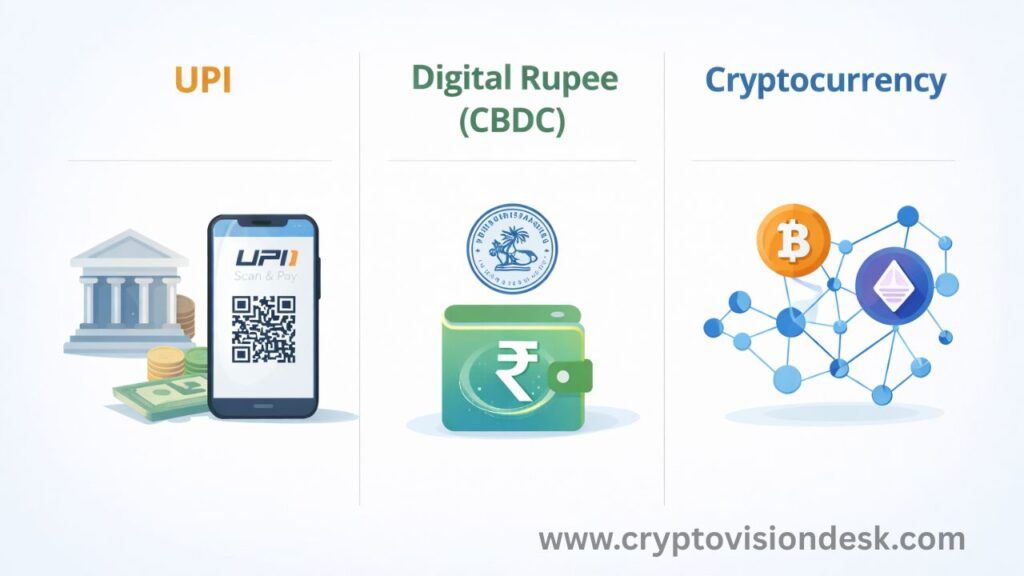

Digital Rupee vs UPI vs Crypto: What Indian Users Must Know in 2026

This is where most beginners get confused, especially if they already trade coins.

UPI vs Digital Rupee: Same phone, very different money

UPI is a payment system. It moves money between bank accounts.

Digital Rupee is the money itself, issued by RBI, stored in a CBDC wallet.

In a shop:

- With UPI: your bank account sends money to the merchant’s bank account.

- With e₹: your CBDC wallet sends e₹ to the merchant’s CBDC wallet. Settlement is final in central bank money.

UPI funds in your savings account can earn interest. e₹ in your wallet does not.

Digital Rupee vs cryptocurrencies like Bitcoin: Not the same thing

Key points for crypto users:

- e₹ is legal tender, backed by RBI, with a fixed value of 1 INR.

- Bitcoin and other crypto are private assets, not legal tender, with prices that can swing a lot.

- People use e₹ mainly for payments and settlement, not for trading gains.

- On your exchange, CBDC is not a new token to speculate on. It is more like digital cash that can move in and out of accounts or platforms.

What happens to your bank savings and fixed deposits if CBDC grows?

Since e₹ does not pay interest, most people will still keep:

- Salary and savings in bank accounts.

- Long-term money in FDs, PPF, mutual funds, and SIPs.

RBI is aware of the risk that people might shift too much into CBDC. That is why it talks about limits and careful design. Your regular savings and investment products are expected to stay central in your financial life.

Fees, speed, and convenience: Which is better for daily payments?

For you as a user:

- UPI is already fast and usually free.

- e₹ payments are also instant and final.

In some special cases, like wholesale markets or cross-border use, CBDC can cut costs for banks. For daily payments, many people will simply use both UPI and e₹, depending on habit, offers, and which app feels easier.

Benefits, Risks, and Privacy Concerns of India’s CBDC for Small Users

You should see both the upside and the downside, without panic.

Key benefits of the Digital Rupee for everyday Indians

Some potential benefits are:

- Fast, low-cost digital payments in many cases.

- Better access for people with weak banking links.

- Safer government payouts and fewer fake notes.

- A public money option in a world full of private apps.

- Offline features that can help in low network areas.

For many users, e₹ will feel like cash plus UPI combined on one screen.

Privacy and tracking: How visible are your CBDC transactions?

RBI has made it clear that CBDC is not fully anonymous like cash. Transactions are traceable to follow laws against crime and terror funding.

Policy makers are still working on how much data is collected, how it is stored, and who can see what. Ignore extreme claims that “RBI will see every chai you drink”, but treat privacy as a serious topic and follow official updates.

Tech risks: Outages, hacks, and what happens if your phone is lost

Any digital system can face:

- Central server outages.

- App bugs.

- Phone theft or SIM swap fraud.

Reduce your risk by:

- Using strong PINs and screen locks.

- Downloading only official wallet apps.

- Keeping your SIM and email secure.

- Reporting lost phones quickly to your bank or wallet provider.

RBI and banks will set rules for disputes and recovery, but your own behavior still matters.

Scams and fake news: Red flags for CBDC users in 2026

Expect scams like:

- Fake “RBI e₹ airdrop” links.

- Fake wallet apps promising free tokens.

- Calls asking for OTP or PIN in the name of Digital Rupee KYC.

Remember simple rules:

- RBI never asks for your OTP or password.

- Always download apps from trusted stores and official bank links.

- Trust RBI, banks, and well-known financial channels, not random Telegram or WhatsApp groups.

How much CBDC should you actually use as a small investor?

Treat e₹ mostly as money for spending and short-term use, not as a place for all your savings.

Balanced habits can look like:

- Keep daily and weekly spending money in e₹ or UPI-linked accounts.

- Keep emergency funds, FDs, PPF, and long-term investments in regulated products.

- Use your exchange for planned investing, not for chasing every new token or rumor.

CBDC is a payment tool, not a full replacement for a sound financial plan.

Read Also: How to Earn Bitcoin: 15 Real Ways That Work

Conclusion

The Digital Rupee is RBI’s version of digital cash, sitting beside cash, UPI, cards, and bank accounts. It is different from both UPI, which is a payment rail, and crypto, which is a private and volatile asset class.

In 2026, you can expect a wider yet gradual rollout, with more banks and apps offering e₹, but no sudden ban on cash or UPI. The benefits are real, from cleaner government transfers to offline payments, and the risks are manageable if you stay informed and careful.

Follow RBI and bank announcements, learn to use official CBDC wallets when they reach your area, and keep using a mix of tools that fit your comfort. With basic knowledge and common sense, the Digital Rupee can become one more helpful tool in your Indian payment stack, not something to fear.

Disclaimer:

This article is for educational and informational purposes only. It does not constitute financial, investment, legal, or tax advice. The Digital Rupee (e₹) is currently under pilot and evolving, and features, rules, and availability may change based on RBI and Government of India policies. Readers should refer to official RBI announcements or consult qualified professionals before making financial decisions. The author and publisher are not responsible for any actions taken based on this content.